The Chartered Accountant in London Built for Landlords

Making Tax Digital, Capital Gains Tax, and rental income tax with a dedicated chartered accountant who understands London’s property market inside out. Transparent fees. Expert advice. No surprises.

London Landlords Face the UK's Most Complex Property Tax Landscape

01

Whether you require a straightforward rental income self-assessment, advice on incorporation into a Special Purpose Vehicle (SPV), or strategic tax planning ahead of a property disposal, our chartered accountant services in London are structured specifically around the challenges you face as a landlord.

02

A qualified chartered accountant in London with specialist knowledge of property tax is no longer a luxury — it is an essential tool for protecting your investment, maximising allowable deductions, and ensuring full HMRC compliance. At AccoFirm, our ICAEW-regulated chartered accountants serve landlords holding single buy-to-let properties through to multi-property portfolios across all London boroughs.

03

Managing rental properties in London is not simply a matter of collecting rent and filing an annual tax return. Between Section 24 mortgage interest restrictions, Capital Gains Tax on disposal, Stamp Duty Land Tax surcharges, and the imminent arrival of Making Tax Digital, London landlords are navigating one of the most demanding tax environments in the United Kingdom.

Comprehensive Accountancy & Tax Services for London Landlords

Every service we offer is tailored to the realities of owning and letting residential property in London — not generic accounting wrapped in property language.

Landlord Self-Assessment Tax Returns

Accurate, fully optimised self-assessment returns for landlords. We identify every allowable expense — letting agent fees, repairs, insurance, professional fees — and ensure your rental income is reported correctly, minimising your tax liability within the law.

Buy-to-Let & Property Portfolio Accounting

From a single buy-to-let to a multi-property portfolio across multiple London boroughs, we manage your complete accounting requirements — income tracking, expense allocation, mortgage interest calculations, and annual accounts preparation.

Landlord Self-Assessment Tax Returns

Accurate, fully optimised self-assessment returns for landlords. We identify every allowable expense — letting agent fees, repairs, insurance, professional fees — and ensure your rental income is reported correctly, minimising your tax liability within the law.

Making Tax Digital (MTD) Compliance

Full MTD for Income Tax management for landlords. We set up HMRC-compliant software, establish your quarterly reporting routines, prepare and submit quarterly updates, and file your Final Declaration — so you never miss a deadline or face an avoidable penalty.

Limited Company (SPV) Incorporation Advice

Is a Special Purpose Vehicle right for your property portfolio? We analyse your current tax position, model incorporation scenarios, calculate the SDLT and CGT implications of transfer, and advise on the optimal ownership structure for your specific situation.

Limited Company (SPV) Incorporation Advice

Is a Special Purpose Vehicle right for your property portfolio? We analyse your current tax position, model incorporation scenarios, calculate the SDLT and CGT implications of transfer, and advise on the optimal ownership structure for your specific situation.

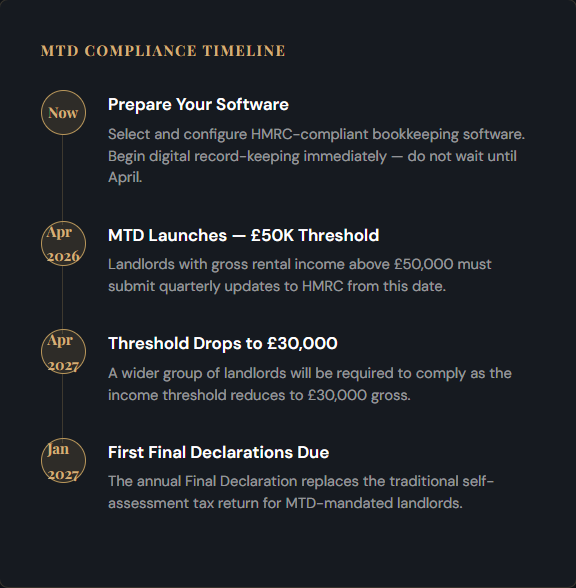

Is Your Rental Income Ready for Making Tax Digital?

Making Tax Digital for Income Tax Self-Assessment (MTD for ITSA) is the biggest change to the UK tax system in a generation. From 6 April 2026, landlords with gross rental income above £50,000 must transition away from the annual self-assessment system and begin submitting quarterly digital updates directly to HMRC.

For London landlords — where average rental yields frequently exceed this threshold — MTD compliance is not optional. The penalties for non-compliance are immediate and accumulative.

- HMRC-approved digital accounting software (Xero, QuickBooks, or FreeAgent)

- Quarterly digital updates submitted every three months

- A Final Declaration submitted by 31 January annually

- Digital record-keeping of every rental income and expense transaction

- Gross income threshold: £50,000 from April 2026; £30,000 from April 2027

Understanding Your Tax Obligations as a London Landlord

London landlords are subject to a layered tax framework that spans income tax on rental profits, Capital Gains Tax on disposals, Stamp Duty Land Tax surcharges on acquisition, and Inheritance Tax on estate planning. Understanding each element — and how they interact — is the foundation of sound property tax planning.

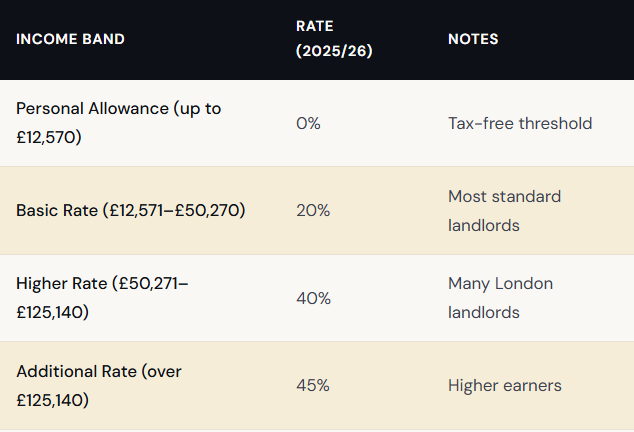

Rental Income Tax: Key Principles for 2025/26

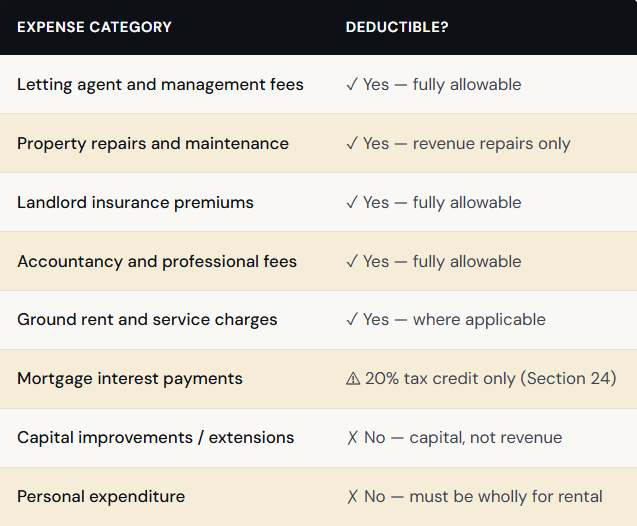

You pay Income Tax on your net rental profit — gross rental income minus allowable expenses. Allowable deductions include letting agent fees, property repairs and maintenance (not capital improvements), landlord insurance, ground rent, service charges, and professional accounting fees. Your rental profits are added to your other income and taxed at your marginal rate.

Section 24: Mortgage Interest Restriction

Individual landlords can no longer deduct mortgage interest as an expense from rental income. Instead, a 20% basic rate tax credit applies to mortgage interest paid. For higher-rate (40%) and additional-rate (45%) taxpayers — which describes a substantial proportion of London landlords — this significantly increases the effective tax burden. A chartered accountant can model whether operating through a limited company would reduce your overall liability.

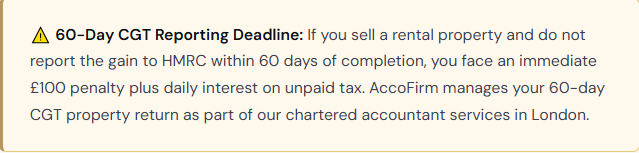

Capital Gains Tax on London Property

When you sell a residential rental property, CGT applies to the gain. For 2025/26, the CGT rate on residential property is 18% for basic rate taxpayers and 24% for higher and additional rate taxpayers. London property values frequently produce substantial gains — a property purchased in Zone 2 for £400,000 in 2015 may be worth considerably more today. You must report and pay CGT within 60 days of completion — a strict HMRC deadline.

Allowable Expenses: What London Landlords Can Deduct

The following costs are deductible against rental income for the 2025/26 tax year, provided they are wholly and exclusively for the letting business:

Tailored Tax Return Services for Everyone

Whether you’re self-employed, employed, or running a small business — we’ve got you covered.

Bank-Level Security

Your personal and financial data are fully encrypted.

Bank-Level Security

Your personal and financial data are fully encrypted.

Bank-Level Security

Your personal and financial data are fully encrypted.

Questions London Landlords Ask Us Most

Do I need a chartered accountant as a landlord in London?

For straightforward rental income from a single property, a general accountant may suffice. However, given the complexity of London property taxation — Section 24 mortgage interest restrictions, Making Tax Digital from April 2026, the 60-day CGT reporting rule, and the potential benefits of limited company structures — a specialist chartered accountant in London with property expertise typically pays for itself many times over through tax savings and penalty avoidance. An ICAEW-regulated chartered accountant also carries professional indemnity insurance and is held to mandatory professional standards, providing significant additional protection.

What is Section 24 and how much will it cost me?

Section 24 (officially the Finance Act 2015, Section 24) eliminated the ability for individual landlords to deduct mortgage interest as an expense against rental income. Instead, you receive a 20% basic rate tax credit on mortgage interest paid. For a higher-rate taxpayer (40%) with a large London mortgage, this can dramatically increase your effective tax bill. For example, a landlord paying £20,000 per year in mortgage interest previously received £8,000 of tax relief at 40%; under Section 24, they receive only £4,000 — a £4,000 annual increase. Our chartered accountants quantify your exact Section 24 impact and identify whether incorporation or other strategies could mitigate it.

What is Making Tax Digital and does it affect me?

Making Tax Digital for Income Tax (MTD for ITSA) is a fundamental change to how landlords report income to HMRC. From 6 April 2026, if your gross rental income (before any expenses) exceeds £50,000, you must use HMRC-approved software to maintain digital records and submit quarterly updates to HMRC — four times per year rather than once. A Final Declaration replaces the traditional annual self-assessment return. From April 2027, the threshold drops to £30,000. In London, where average rents across Zone 1 and Zone 2 properties regularly exceed £4,000 per month, most serious landlords will be affected from April 2026. AccoFirm manages your complete MTD transition — software selection, quarterly submission management, and annual Final Declaration filing.

Should I hold my London rental properties in a limited company?

This depends entirely on your specific circumstances — your current tax rate, portfolio size, mortgage arrangements, and plans for the properties. For higher and additional rate taxpayers with growing portfolios, a limited company (typically a Special Purpose Vehicle or SPV) can offer significant advantages: corporation tax at 19–25% instead of personal income tax at 40–45%, no Section 24 restriction (companies deduct mortgage interest as a business expense), and more flexible profit extraction. However, transferring existing properties into a company triggers Capital Gains Tax and Stamp Duty Land Tax on the transfer — which can be prohibitive. We model both scenarios with your specific numbers before making any recommendation.

What is the 60-day CGT rule for landlords?

If you sell a UK residential rental property that is not your main residence, you are required to report the gain to HMRC and pay the Capital Gains Tax due within 60 days of the completion date. This is entirely separate from your annual self-assessment tax return. Missing this deadline results in an immediate £100 penalty, with further penalties and interest accruing if the delay continues. In London, where property values can generate substantial gains, the CGT liability can be considerable. AccoFirm calculates your gain, identifies all available reliefs, prepares the 60-day return, and ensures it is submitted accurately and on time.

How much does a landlord accountant in London cost?

AccoFirm charges fixed, transparent fees that are agreed in writing before we begin any work. The cost depends on your portfolio size, the range of services required, and the complexity of your tax affairs. A self-assessment tax return for a landlord with a single buy-to-let property will cost considerably less than a full quarterly MTD compliance service for a portfolio landlord with five or more properties plus limited company accounting. We never charge by the hour for standard landlord accounting services — you always know exactly what you will pay. Contact us for a bespoke, no-obligation quote.

Can AccoFirm help with HMRC investigations and landlord compliance checks?

Yes. HMRC regularly conducts compliance checks on landlords — particularly those who have been slow to register rental income, have made errors on previous returns, or have been flagged through the Let Property Campaign. Our chartered accountants represent you throughout any HMRC enquiry, handle all correspondence, prepare voluntary disclosures where appropriate, negotiate settlement terms, and work to minimise any penalties. If you are contacted by HMRC regarding your rental properties, seek professional advice immediately.